New IRS 1099-DA Is Here — It Might Tell the IRS You Sold Before You Know What You Owe

What the new 1099-DA actually does (and what it doesn’t)

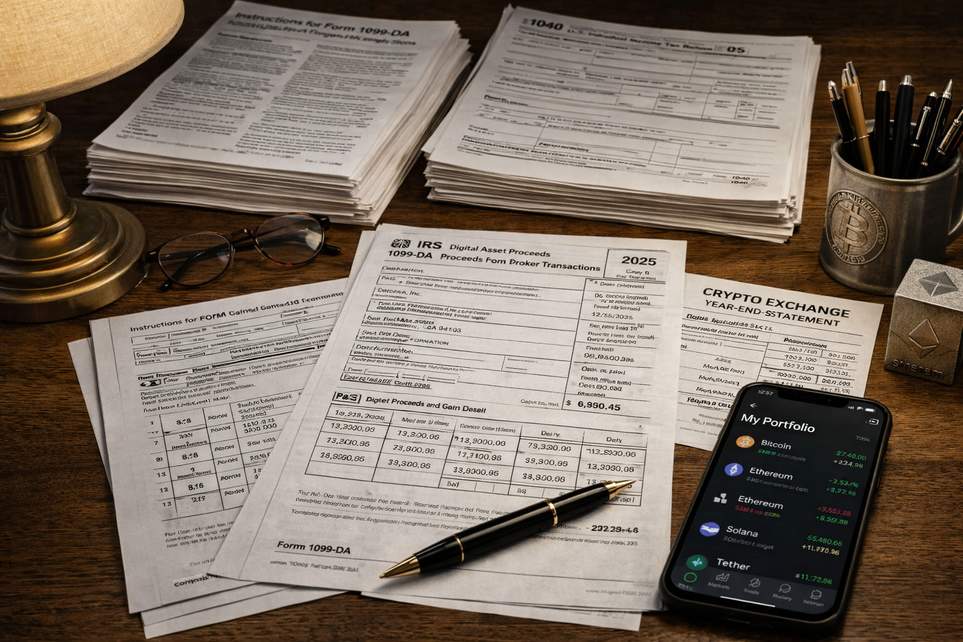

Heads up: the IRS rolled out Form 1099-DA for 2025 crypto activity, and a lot of investors are finding one in their inbox before they’ve done the math. In plain terms, brokers will be reporting gross proceeds from many digital-asset disposals this year. But “reported proceeds” does not automatically equal “tax bill settled.”

Why the confusion? For the transition year, many statements will list the dollars you received when you sold or moved assets, but they often won’t include the cost basis — the number you need to figure out whether you actually made a gain, took a loss, or barely broke even. If you moved coins between wallets or across platforms, or you sold something that was originally acquired elsewhere, that basis detail may be missing.

The IRS treats digital assets as property. That means you can trigger a taxable event not only by selling for cash, but by exchanging for another coin, using crypto to buy goods or services, or even paying broker fees in crypto. The new form is really an alert that a disposition happened — a flag on the government’s radar — not a final, hand-delivered invoice for taxes due.

Why you should care and what to do (no panic, just paperwork)

Surveys show a lot of people know crypto can be taxable, but many don’t know when taxes actually kick in. Plenty of investors hop between platforms and self-custody wallets — the average user in one industry survey reported using a couple of platforms and moving assets around frequently — and that makes tracking basis messy. Many folks assume a bank transfer or a simple account move is taxable when it may not be, while others think a sale only matters once profits cross some magical threshold.

Bottom line: don’t treat Form 1099-DA like a complete brokerage statement. Tax pros are already saying the same thing — this form is a signal, not the whole story. You are still responsible for calculating cost basis, establishing holding periods, and reporting gains or losses correctly even if your 1099-DA lacks that basis information.

What to do right now: tighten up your records. Record purchase dates and prices, keep track of transfers (where and when coins moved), export trade histories and wallet transaction CSVs, and note whether an asset was acquired on a platform or via private transfer. If the numbers on your 1099-DA don’t match your own logs, expect to do some detective work — accountants are already performing “forensic reconciliation” rather than simple form-matching this year.

If you use multiple platforms or a mix of exchanges and self-custody wallets, a little organization goes a long way. Tax software that supports crypto can help, but it’s not magic: you still need clean source records. And if you’re unsure, ask a tax professional — especially if your 1099-DA shows proceeds but you don’t see the matching basis.

Finally, be aware of platform rules: some brokers may include consent language during onboarding and could restrict accounts for those who refuse certain electronic notices. That’s separate from the tax rules, but it affects how exchanges communicate these forms and what options you have for receiving them.

In short: the new form gives the IRS a clearer window into many crypto sales, but it doesn’t absolve you of the homework. Keep receipts, export your histories, and don’t let a single line on a form lull you into thinking the tax job is already done.