Hyperliquid’s $1B HYPE Bet Meets Thin Liquidity — Hold On to Your Hats

Quick rundown

Hyperliquid Strategies built a public-company treasury around the token HYPE and lined up a massive equity facility so it can keep buying more. The company has the ability to sell up to $1 billion worth of its own stock (timing controlled by Hyperliquid) to fund ongoing token purchases.

The plan started with a PIPE that included roughly $300 million in cash plus about 12.5 million HYPE tokens. Those tokens were worth far more when the deal was signed than when the books closed — a paper loss in the hundreds of millions before the firm bought another token. By mid-May the company reported holding roughly 20.8 million HYPE, which it said was the largest HYPE stake among U.S. public companies.

On top of that, a separate filing from a big asset manager proposed a publicly offered staking vehicle that would hold HYPE directly and potentially stake it. That filing notes practical limits: the trust can’t sell while the registration is still pending, staking and unstaking take time, and those timing windows matter most when markets get spicy.

The messy mechanics (and the eyebrow-raising details)

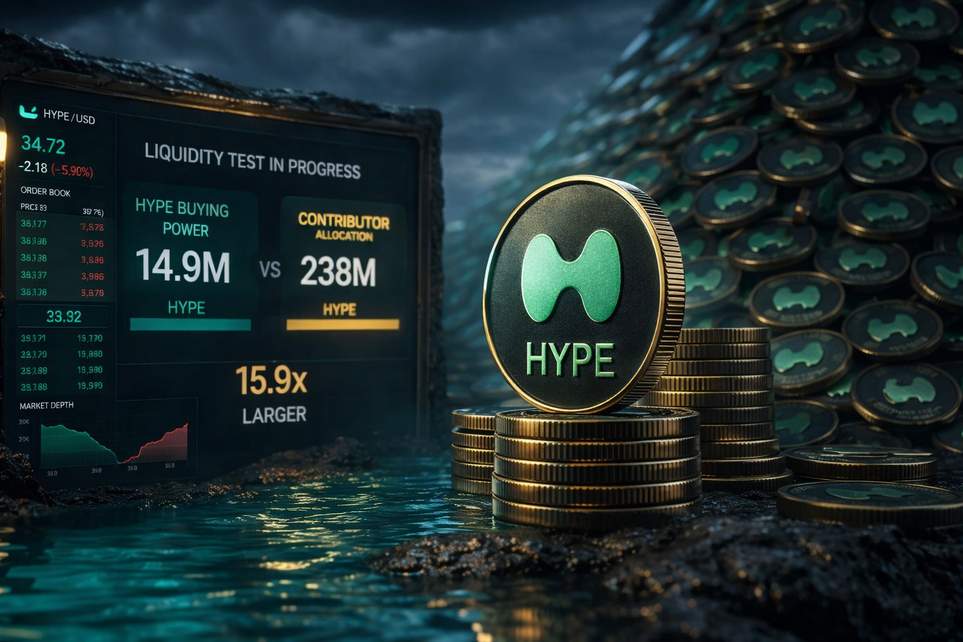

There are a few moving parts making this feel like juggling flaming chainsaws. First, the token supply is capped at one billion HYPE. About 310 million were unlocked at launch, roughly 238 million are allocated to core contributors on a multi-year monthly vesting schedule, and a few hundred million are earmarked for future rewards. That core allocation alone is huge — at recent prices it dwarfs the $1 billion stock facility the company can tap.

If Hyperliquid used the whole $1 billion buying line, they’d pick up around 14.9 million HYPE — roughly 1.5% of total supply and about three-quarters of what they already own. Monthly vesting from core contributors could put several million fresh tokens into circulation every month, a number that is large relative to Hyperliquid’s stated buying capacity.

Market structure adds another wrinkle. Perpetual futures markets around HYPE show enormous turnover: open interest is a very large slice of the token’s market cap, daily and monthly trading volumes are massive compared with that open interest, and liquidation flows are nontrivial. Translation: the token trades in a high-leverage, high-liquidation environment that can move prices fast.

On the validator side, Hyperliquid runs a relatively small set of validators. The filings point to a handful of real incidents where fast, coordinated responses by validators helped contain problems — and also raised centralization alarms. There were at least two market meltdowns on record where price-manipulation attacks and rapid validator actions led to millions in losses and emergency protocol responses, including brief halts in withdrawals.

Two possible futures (pick your vibe)

Upside scenario (the “smooth jazz” path): Hyperliquid sells stock at reasonable prices, uses proceeds to buy more HYPE, staking yields make holders stickier, and the token’s market cap grows faster than liquidation pressure. A public staking product launches smoothly, spreads stay tight, and HYPE starts behaving more like a credible, tradeable treasury asset.

Downside scenario (the “roller coaster” path): The token’s price tumbles as leverage and liquidations spike, the company’s shares trade below their net-asset value, and raising more stock becomes painfully dilutive. Spot liquidity thins, authorized participants struggle to hedge new fund shares, monthly vesting becomes a price-moving event, and the public-market wrappers end up amplifying volatility instead of calming it.

In short: the corporate vehicle and the proposed public staking product both give regular investors access to a token whose own documentation admits there may be times it’s hard to sell. That makes the whole experiment fascinating, risky, and a little bit theatrical. Bring popcorn, but maybe keep your seatbelt on.

Author note: reporting and filings show the facts above; this summary paraphrases and simplifies those details for a breezy read, not investment advice.