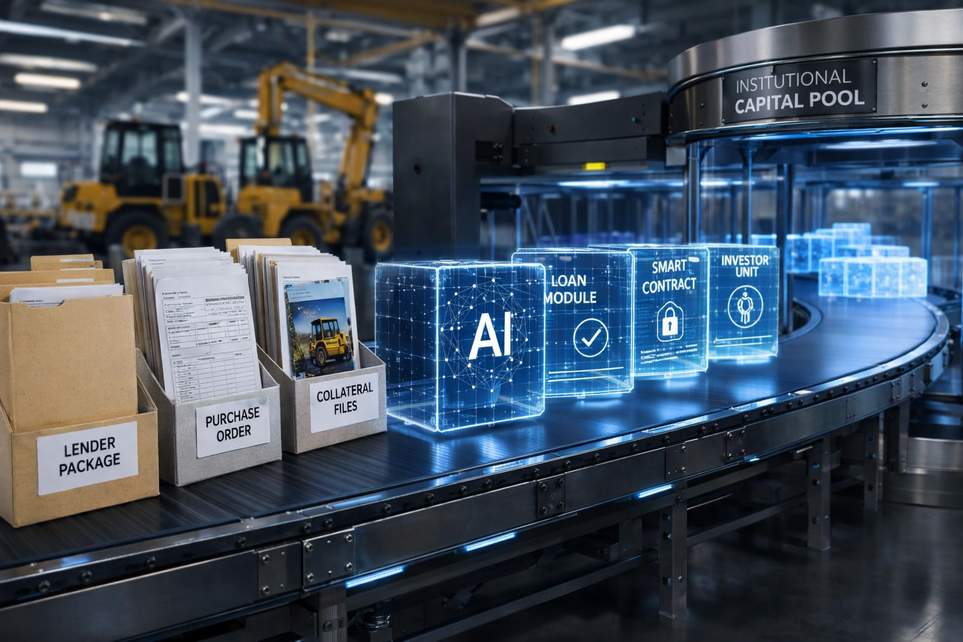

Lenders Want AI to Turn Months of Paperwork into One-Day On-Chain Equipment Loans

Imagine turning a mountain of loan paperwork into something that signs off before you finish a sandwich. That’s the pitch: two finance tech teams are trying to shove roughly $650 million of equipment loans onto blockchain rails over four years, using AI to do the heavy lifting — risk checks, due diligence, pricing — and squeeze a months-long origination process into a single business day for small and mid-sized companies.

The one-day loan idea

Here’s the short version: the target borrowers are businesses buying equipment in fields like manufacturing, industrial electrical work, and residential solar. AI is meant to comb purchase orders, borrower records, credit inputs, and equipment details, stitch them together with lender rules, and spit out a risk decision fast enough that a loan goes from application to funded in a day. The blockchain piece is mainly about recording ownership slices and letting investor exposure move on programmable rails — tokenized access, if you like — while the underlying loans might still be funded and serviced in traditional ways.

In practice this looks hybrid at first: institutional lenders may fund loans off-chain while a tokenized liquidity vehicle provides on-chain investor exposure to parts of the deals. Tokenization can make investor records cleaner and transfers more automated, but it doesn’t magically solve legal knotty bits like lien paperwork, insurance, repossession, or how recovery works when things go sideways.

Why this could be awesome — and why it might bite you

Why it’s exciting: accelerate approvals, give businesses faster access to capital, and make investor ownership records neat and auditable. There’s a real market here — industry data suggest over a trillion dollars of equipment and software investment in the U.S. is financed every year — so even a modest slice matters as a proof of concept.

Why it’s risky: automation is only as smart as the data and models behind it. If AI misses dodgy borrower finances, inflated equipment valuations, or shifting sector conditions, speed just means losses land faster. Equipment loans hinge on borrower cash flow, resale markets for physical assets, enforceable liens, servicing quality, and recovery mechanics — all things that live outside a blockchain token.

So the experiment will hinge on a few signals: whether underwriting automation actually improves file quality, how transparent and useful on-chain performance data is, who runs the tokenized pool, and how governance of the AI and legal frameworks are handled. Loan seasoning — delinquency, loss, and recovery over time — will be the real scoreboard.

Bottom line: AI plus blockchain could make equipment financing feel like buying a new laptop online instead of wrestling with a filing cabinet and fax machine. But until we see disclosures about the token operator, AI controls, and actual loan performance over time, treat the one-day promise as an intriguing prototype rather than a done deal.